Key points

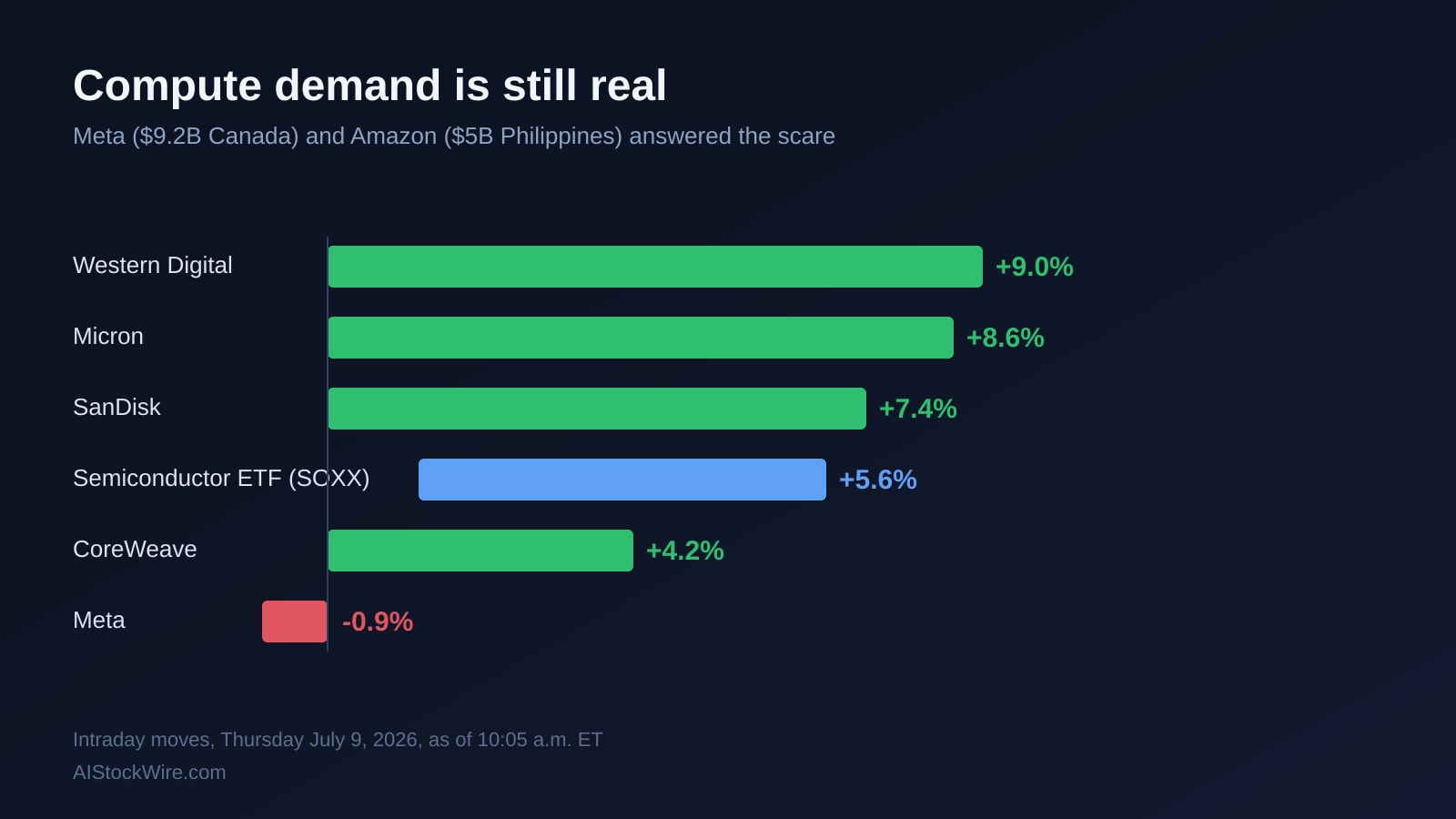

- Micron (MU), Western Digital (WDC), and SanDisk (SNDK) are up 7% to 9% Thursday morning, their best day since a chip-sector scare started a week ago.

- The scare began July 1, when a report that Meta was building a business to sell "excess" AI computing power spooked the whole AI trade, sinking CoreWeave (CRWV) 13.9% and Nebius (NBIS) 17% in a single session.

- Samsung then posted the largest quarterly operating profit any tech company has ever reported. Its stock fell about 7% anyway, because investors already suspected the top was in.

- This week, Meta and Amazon (AMZN) each answered with real money: a C$13 billion ($9.2 billion) data center in Alberta, Canada, and a $5 billion commitment to the Philippines. Today's rally is the market betting they're right.

Micron, SanDisk (SNDK), and Western Digital (WDC) are having their best day in weeks Thursday, up 7% to 9% apiece. A week ago, memory and chip stocks were doing the opposite, sliding on fear that AI infrastructure spending was starting to top out. What changed in between was not a new rumor. It was two of the biggest spenders in AI, Meta Platforms (META) and Amazon (AMZN), each committing billions of dollars to new data centers this week. Compute power is still needed, and the market is reacting to that, not to talk.

Today's rally, by the numbers

As of 10:05 a.m. ET Thursday, before the closing bell, here is where the group stands. These are live, intraday figures and will move before the close:

| Stock / fund | Move vs. Wednesday close |

|---|---|

| Western Digital (WDC) | +9.0% |

| Micron (MU) | +8.6% |

| SanDisk (SNDK) | +7.4% |

| iShares Semiconductor ETF (SOXX) | +5.6% |

| VanEck Semiconductor ETF (SMH) | +4.0% |

| CoreWeave (CRWV) | +4.2% |

| Nebius (NBIS) | +2.6% |

| Nvidia (NVDA) | -1.5% |

| Meta (META) | -0.9% |

Meta slipping while its suppliers rally is a pattern that has now shown up twice this week: the company doing the spending gives a little back while the companies getting paid for that spending catch a bid. Nvidia's small dip is a reminder this bounce is concentrated in memory and storage names specifically, not chips broadly.

How the scare started

Rewind to July 1. Bloomberg reported that Meta was building an internal effort, reportedly called Meta Compute, to sell excess AI capacity to outside developers. Meta declined to confirm it. The market did not wait for confirmation. CoreWeave fell 13.9% and Nebius dropped 17%, losing about $12 billion in value in a single session, on fear that Meta, one of their biggest customers, could rent less if it started selling its own spare capacity instead. Chip and infrastructure names sold off with them, on a simple and alarming piece of logic: if the company spending the most on AI computing power thought it had too much, maybe the whole buildout was further along than anyone realized. We covered that day in our full piece on Meta's Alberta data center.

Korea's memory chip stocks had a rough week too, on their own overlapping timeline. The Kospi fell about 8% on July 2, with SK Hynix down over 14% and Samsung down about 9% in a single session, together losing roughly $290 billion in value. That decline landed the same week as the Meta scare and got lumped in with it in some same-day coverage, but our own reporting at the time traced Korea's slide to its own separate worries about memory pricing and spending. Two scares, overlapping in time, are not the same scare, but both fed the same underlying question.

Samsung's record quarter that couldn't shake the fear

Samsung supplied the clearest test of that question on July 7. It guided to 89.4 trillion won in second-quarter operating profit, about $58.4 billion, up roughly 18-fold from a year earlier. According to Bloomberg, that is the largest quarterly operating profit any technology company has ever reported, ahead of anything Nvidia or Apple (AAPL) has posted. By any normal reading, that is proof AI-driven memory demand is not slowing down. Samsung's stock fell about 7% anyway. Revenue of roughly 171 trillion won came in a bit below analyst estimates, and Samsung shares had already run up about 150% over the prior twelve months on this same story, so the print had little new to offer buyers. But the deeper reason was the fear the Meta report had planted a week earlier: with that story still fresh, investors treated even a record-breaking quarter as a signal that this was as good as it gets, not a reason to buy more.

Two hyperscalers bet billions that the fear was wrong

The question got a real answer this week, in the form of money committed, not statements made. On July 8, Meta broke ground on a C$13 billion (about $9.2 billion), 1-gigawatt data center in Alberta, its largest anywhere outside the US, and signed up for an entirely new gas-fired power plant just to feed it. A company that genuinely believed it had too much compute would not be doing that.

The same day, Amazon Web Services committed $5 billion over 15 years to build out data center capacity in the Philippines, a market it had pointedly left out of a separate $33 billion, four-country Southeast Asia pledge made just seven weeks earlier, in May. When AWS excludes a country from one investment plan and then commits real money to it two months later, that is demand showing up faster than the original plan accounted for, not a company hedging its bets. Neither announcement was about memory chips directly, but both are about the thing memory chips feed: more data centers mean more demand for the DRAM, NAND, and high-bandwidth memory that Micron, SanDisk, Western Digital, Samsung, and SK Hynix all sell into. That is the read-through the market is making Thursday.

This is a bounce, not a new high

It is worth being precise about what Thursday's move is and is not. Semiconductor stocks as a group remain well below their recent highs, and the sector was in a double-digit correction before this bounce started. This is chip and memory names clawing back part of a bad stretch, confirmation the demand story survived a scare, not proof the scare never mattered. The broader market also has a second, unrelated headwind: an escalating US-Iran conflict, after the White House said the ceasefire was over, pushed oil prices up more than 4% Wednesday, and Brent crude was still climbing early Thursday on reports of tanker attacks in the Strait of Hormuz, keeping overall trading choppy. Chip stocks are up because of a chip-specific story. The rest of the market is dealing with a different one at the same time.

What's next

SK Hynix is set to begin trading on the Nasdaq Friday, July 10, under the ticker SKHY, in a roughly $29 billion ADR listing that values the company near $1 trillion. It is the most direct real-time test yet of whether US investors believe the compute demand story, arriving one day after this week's reversal.

None of this settles the argument for good. Samsung's own guidance still has to convert into an actual earnings report later this month, and the capital spending questions that knocked its stock down on July 7 have not gone away. But the week's actual capital commitments, not comments on an earnings call or an unconfirmed report, point the same direction. A rumor said the AI buildout might be slowing down. Meta and Amazon both spent real money this week proving otherwise, and Thursday's rally is the market reacting to the money, not the rumor.