Key points

- The part of an option's price that isn't already in the money decays on a curve that bends hardest in the final days before expiration. That's what's really behind the "Friday feeling."

- A 2005 academic study found real, measurable clustering of stock prices near heavily traded strikes on expiration dates, an average 16.5 basis point shift and about $9 billion in market value moved on a typical expiration day.

- The study's own explanation is market-maker hedging. Nobody is choosing a number in a meeting to hurt option buyers.

- When your contract expires worthless, whoever sold it to you keeps your premium. Most of the time that's just another trader or a fund collecting income, nothing aimed at you specifically.

Every options trading forum has a version of the same theory: institutions wait for Friday, then gang up to make retail contracts expire worthless on purpose. A contract looks fine Wednesday. By Friday afternoon it's worth half as much and the stock hasn't even moved. Something clearly did that, or so it feels. The real cause is boring math and routine hedging, and once you see the mechanism, the Friday pattern stops looking like a conspiracy and starts looking like something you can plan around.

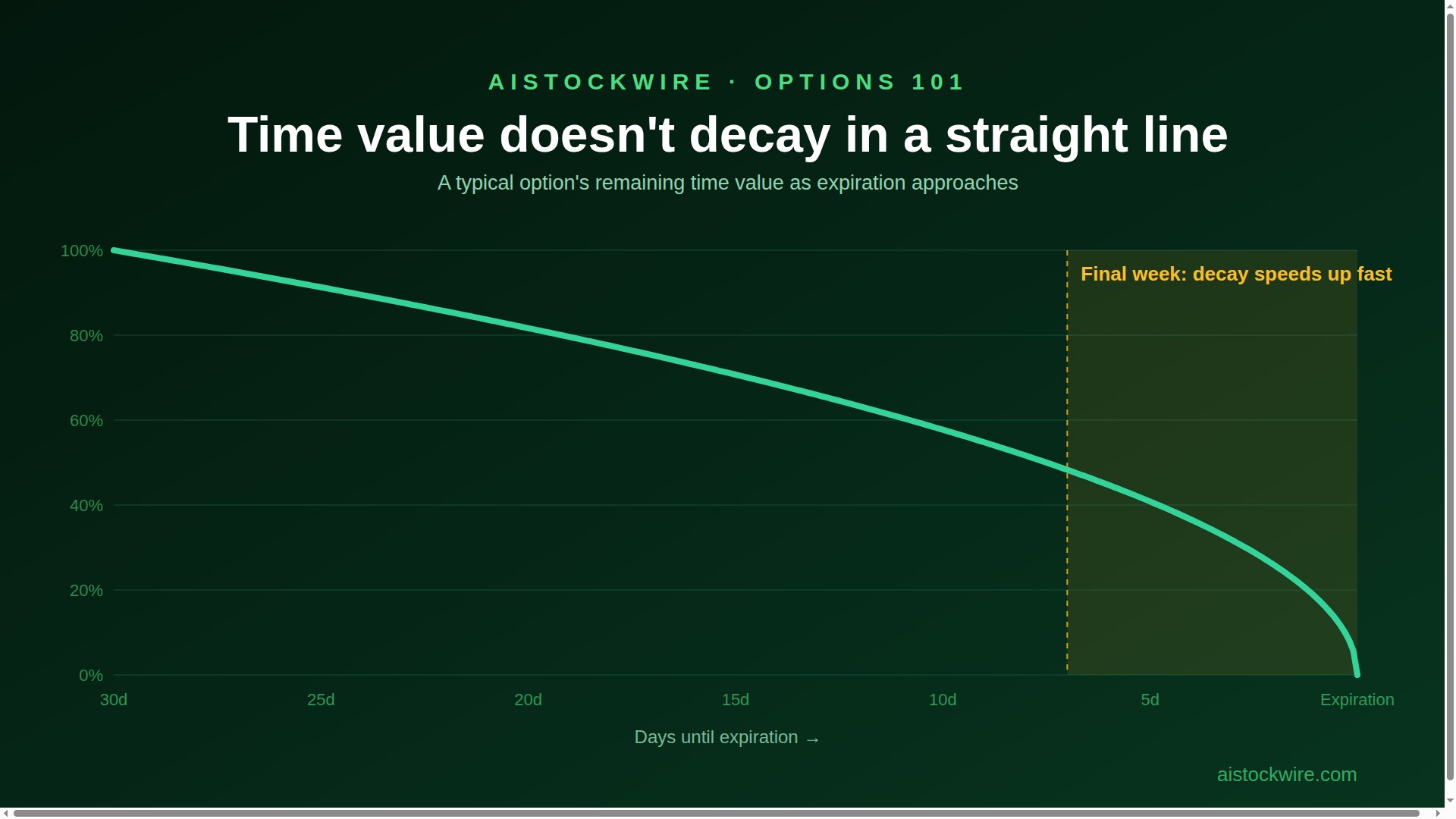

The decay is real, and here's exactly how fast it happens

Only the piece of an option's price that isn't already locked in, its time value, changes on its own as the calendar moves. Think of time value as pure hope: what a buyer pays for the chance the stock still moves their way before the clock runs out. That hope only shrinks, and it doesn't shrink in a straight line. Cboe's own options-education material lays out the math in full, but the short version is this: a contract with a month left might lose a few cents of that hope per day. The same contract with two days left can lose that much before lunch. Buy Monday and hold through the week, and you spend the entire stretch sitting in the steepest part of that curve. A flat stock and a shrinking contract at the same time just means you landed in the steep part of it.

What the "max pain" data shows

The folk theory says a stock drifts toward whichever strike would inflict the biggest combined loss on option holders on expiration day, the strike where the most calls and puts together end up worthless. That part got tested for real. A 2005 paper in the Journal of Financial Economics, by Sophie Ni, Neil Pearson and Allen Poteshman, tracked stocks with listed options and found genuine clustering near strike prices on expiration dates: an average 16.5 basis point shift in returns and roughly $9 billion in aggregate market value moved on a typical expiration day. The clustering checks out.

Where the forum version goes wrong is the story attached to it. The paper's own answer for why it happens is duller than a conspiracy: delta hedging. Market makers who sell options offset their own risk by trading the underlying stock, and as expiration nears, that hedging gets more sensitive to every tick and clusters around whichever strikes are carrying the most open contracts, a sensitivity traders call gamma. Thousands of routine hedge adjustments landing in the same place at the same time is what pulls the price, mechanical and boring the whole way down.

Who profits when your contract expires worthless

Whoever sold it to you. That's the whole structure of the trade. The seller pockets your premium up front and keeps every cent of it if the contract expires worthless, and that seller could be a market maker, a hedge fund, or just another trader who took the other side of your order. Selling options for income is a common, everyday strategy that has nothing to do with what day of the week it happens to be, and nothing to do with you specifically.

Most options never even make it to expiration. Traders on both sides tend to close out early rather than ride a position to the final bell, and a good chunk of what does run to expiration ends up worthless simply because the stock never cleared the strike. Out-of-the-money options need a real move to be worth anything, and most weeks the market just doesn't hand you one.

What this means for how you trade

Here's the practical takeaway. Time value decays fastest in exactly the window most people are holding a contract into expiration. Market makers hedging their own routine risk can create real, measurable pinning around popular strikes, and nobody there is aiming it at you. Hold something into a Friday expiration and expect the time-value bleed to speed up even on a dead-quiet day. Don't be shocked if the stock drifts toward a strike loaded with open interest. Math did that, and so did a few thousand hedging desks doing their jobs.

Frequently asked questions

Do market makers deliberately make options expire worthless?

No evidence points to deliberate coordination against individual traders. Market makers hedge their own risk by trading the underlying stock, and that routine hedging creates real price pressure near heavily traded strikes. Researchers have documented the pressure itself. An intent to target retail buyers specifically has never been documented anywhere.

How much of an option's value can disappear in the final days before expiration?

It depends on the contract, but the decay curve is steep enough that a position with little intrinsic value can lose a large share of its remaining price in just its last two or three trading days, even if the stock barely moves. That's why a contract can look flat on the underlying and still bleed value fast heading into Friday.

What did the 2005 max pain study actually measure?

Ni, Pearson and Poteshman looked at stocks with listed options and measured how much their closing prices clustered near strike prices specifically on expiration dates versus other days. They found an average 16.5 basis point shift in returns and estimated about $9 billion in aggregate market value moved on a typical expiration day, and attributed the effect to market-maker hedging rather than intentional price-steering.

Do most options expire worthless?

A large share do, mainly because most contracts are bought out of the money and need a specific move to gain value before time runs out. Many other positions get closed before expiration rather than held to the end, so "expires worthless" and "loses money" aren't exactly the same group of trades.

Sources

- Cboe: options education on time value, theta and the Greeks

- Sophie Ni, Neil D. Pearson, Allen M. Poteshman, "Stock Price Clustering on Option Expiration Dates," Journal of Financial Economics, 2005

- Our earlier explainer: what the VIX actually measures

- Our AI investing glossary, for other terms like this one

This is a general explanation of options mechanics, not investment advice. Options trading involves substantial risk and isn't suitable for every investor. Always do your own research and consider speaking with a licensed financial professional before making any investment decision.