Key points

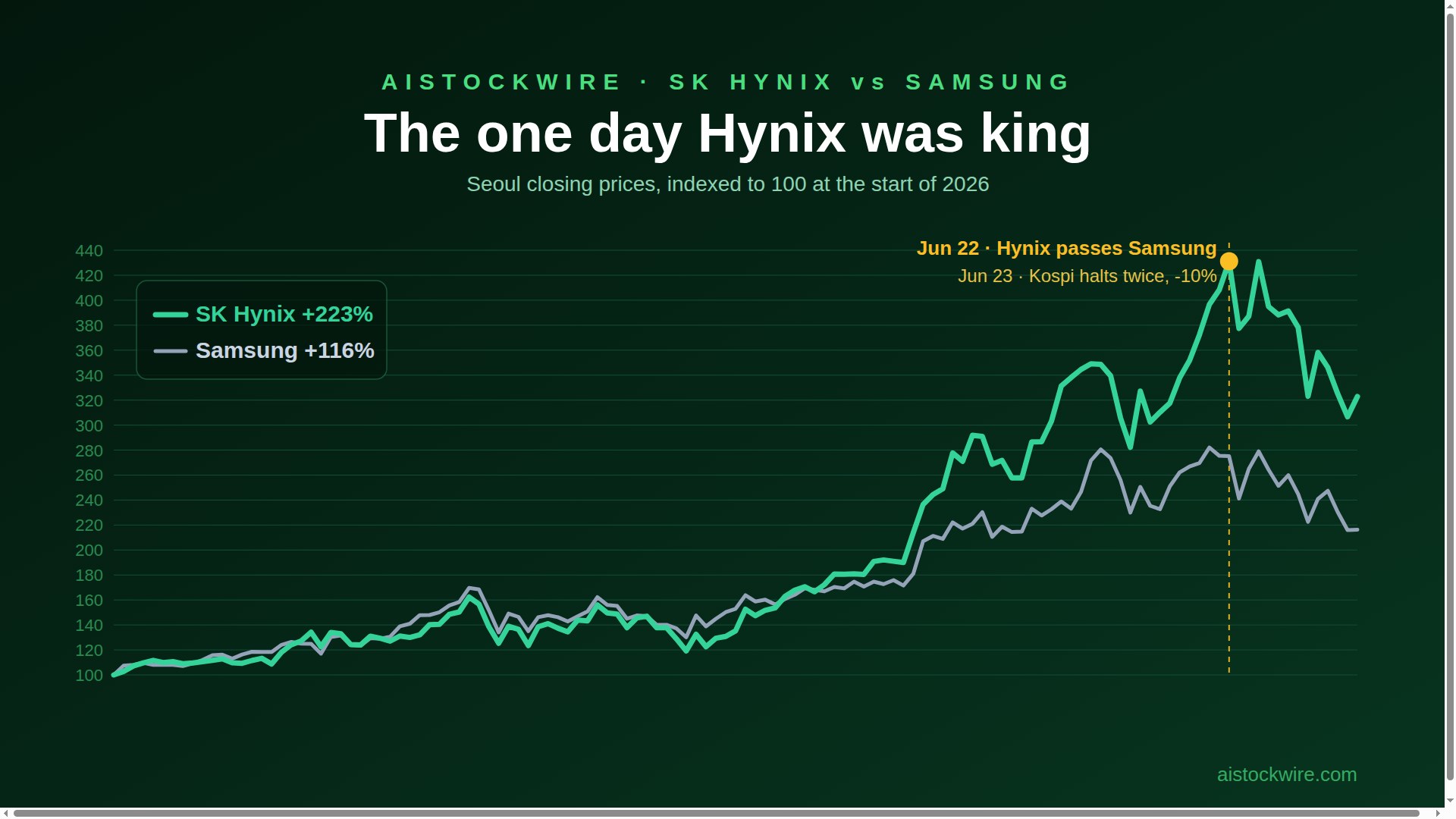

- On June 22, SK Hynix passed Samsung as Korea's most valuable company for the first time in 25 years and 7 months. It lasted one day. The next session the Kospi fell nearly 10%, circuit breakers fired twice, and Samsung was back on top.

- My theory, and it's just my theory: Korea's market is structured so nothing stays above Samsung, and SK Hynix knows it. That's why a $28 billion US listing went from confidential SEC filing in March to trading in July.

- The numbers behind the move: Q1 revenue of $35.5 billion at a 72% operating margin, roughly $169 billion in projected 2026 operating profit, and 10% of that going straight to employees with no cap, tracking near a $477,000 average bonus per person this year.

- The debut lived up to the hype. SKHYV's opening cross printed its first trade at $170, more than 14% above the $149 IPO price, spiked to $176, dropped as low as $166, and has been chopping in the low $170s since. I bought the dip, at a worse price than I wanted.

SK Hynix started trading in New York today under the temporary ticker SKHYV. The deal priced at $149 with about $171.5 billion in orders for $26.5 billion of stock, and once Nasdaq's opening cross finished chewing through the order book, the first trade printed at $170. It spiked to $176, dropped to $166, and has been chopping in the low $170s since. I bought in on that dip. Everyone's watching what it does today. I think the better question is why a company this size sprinted to America in four months. Here's my theory. Write it down and hold me to it.

The one day Korea had a new king

On June 22, SK Hynix passed Samsung in market value during the trading day. Roughly $1.35 trillion against $1.34 trillion. That had not happened in 25 years and 7 months. Samsung is not just a big company in Korea. It's the anchor tenant of the entire market, and for one day the memory company from Icheon was worth more.

It lasted exactly one day. The next session the Kospi fell nearly 10% and closed at 8,203.84. Circuit breakers fired twice in a single day. SK Hynix dropped about 12.5%. Samsung fell hard too, but when the dust settled Samsung was back on top, and it has stayed there since. And here's the detail that gets me: the Kospi's all-time closing high, 9,114.55, came on June 22. The exact day SK Hynix took the crown. The whole market peaked the day the order flipped, then broke so hard they had to stop trading. Twice.

My theory

The official explanation is fine. AI valuations got scary, Wall Street wobbled, leveraged retail money in Korea unwound all at once, and the selling fed on itself. I'm not arguing with any of that. Mechanically that's what happened.

But here's what I believe underneath it. In Korea, nothing gets to stay above Samsung. I'm not claiming some committee makes a phone call. I'm saying the market itself is built around Samsung being number one. The pension money is organized around it. The index products are organized around it. The national pride is organized around it. When the order flipped, the system rejected it like a bad organ. You can tell me the timing is a coincidence. Maybe it is. But if I'm running SK Hynix and the one time my stock proves it can outrank Samsung the entire market crashes and halts within 24 hours, I hear the message loud and clear. You can be big here. You cannot be first.

So you go somewhere that loves crowning a new number one. That's America's favorite sport.

The company acted like it agrees with me

Look at the speed. SK Hynix filed confidentially with the SEC around March. Marketing launched July 6. It priced July 9. It's trading July 10. For a $28 billion raise, the largest first-time US fundraising by any foreign company ever, that is a dead sprint. Companies don't move like that unless somebody senior wants it done yesterday.

The polite name for the problem is the Korea discount. Korean-listed companies trade cheap because of governance worries, thin foreign access, and index exclusion. HSBC put a number on it: Micron has traded at an average 35% premium to SK Hynix over the past 13 years. Same industry. Hynix is the one with roughly 57% of the high bandwidth memory market that feeds Nvidia, and it was the one trading at the discount, mostly because American money couldn't own it without jumping through hoops. The $171.5 billion order book, more than 7 times the deal, tells you how much of that demand was just sitting there waiting for access.

The math that makes this insane

First quarter revenue was 52.58 trillion won, about $35.5 billion, up 198% from a year ago. The operating margin was 72%. Not a typo. A company that manufactures physical objects in giant factories ran a 72% operating margin, which is software economics on hardware volume.

Analysts have 2026 operating profit around 250 trillion won, roughly $169 billion. Hold Q1's margin against that and you're implying revenue somewhere in the $230 to $240 billion a year zone. Run my back-of-envelope on it: call it $240 billion in revenue, roughly 70% of it operating profit, and 10% of that profit goes straight to employees. That last part is real and it's my favorite fact in the whole story. The union deal gives workers 10% of operating profit with no cap, locked for 10 years. Around 35,000 people are tracking toward an average bonus near $477,000 this year. A memory company is paying its whole building like a hedge fund. It's so profitable it's honestly stupid.

Now the part where I keep myself honest. Margins like that are a flare gun to every competitor and every capacity planner on earth. Memory has always been a cycle, and this is what the very top of the good part looks like. I'm not buying because I think 72% margins are permanent. I'm buying because the demand is real, the product lead is real, and the stock finally trades in a market that will pay for it.

What I'm doing

Bought in, like I said when I laid out the thesis last week, just at a worse price than my $160 limit wanted. Nasdaq's opening cross doesn't wait around for your patience. Watching Micron (MU) closely from here, because the US finally has a direct HBM pure play to trade against it and sympathy runs in both directions. And watching Seoul, because if Samsung keeps the crown at home while SK Hynix gets paid in New York, that tells you everything about why this listing happened the way it did.

Sources

- KED Global: How SK Hynix rewrote Kospi history

- Fortune: SK Hynix briefly tops Samsung as Korea's most valuable company

- CNBC: SK Hynix debuts on Nasdaq. Will that narrow its Korea discount?

- SK hynix 1Q26 financial results

- TrendForce: SK hynix 10% profit-sharing on record earnings

- Our coverage: the $149 pricing and why SKHYV shows halted this morning

- Price data via Robinhood market data

This is David's personal opinion and a record of his own trading plan, not investment advice. Figures are as of midday July 10, 2026 and will move. Always do your own research and consider speaking with a licensed financial professional before making any investment decision.