Key points

- HBM (high bandwidth memory) is stacked memory built for AI chips. Every serious AI accelerator, including Nvidia's, depends on it, and suppliers reportedly had 2026 output committed before the year began.

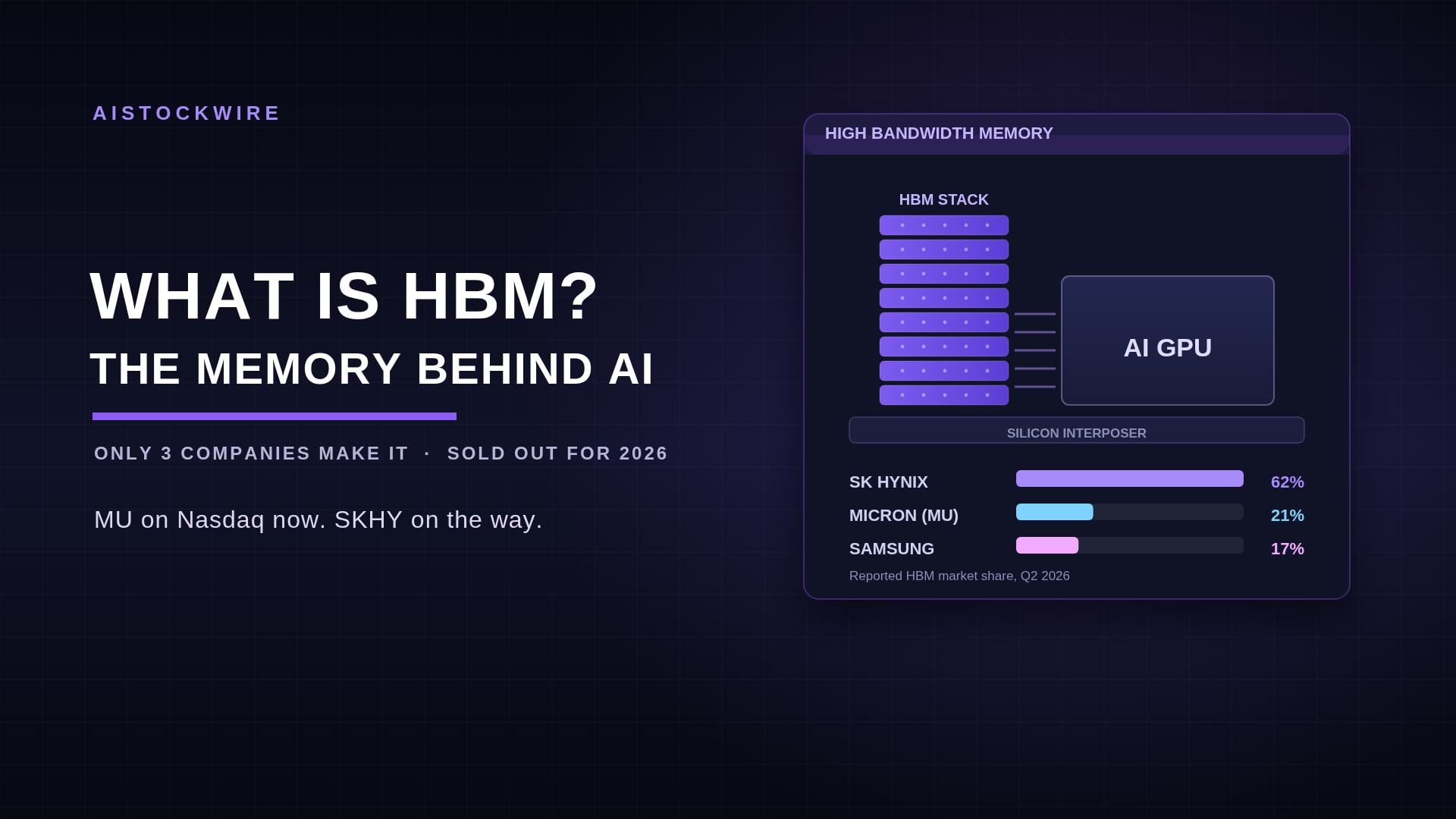

- Only three companies make it: SK Hynix with a reported 62% share, Micron (MU) at 21%, and Samsung at 17% as of mid-2026. Micron recently passed Samsung for the number-two spot.

- Memory went from a boring cyclical business to the center of the AI trade. Micron rose about 304% in the first half of 2026 and SK Hynix roughly 280% on its home exchange.

- US investors can buy Micron on the Nasdaq today, and SK Hynix is arriving there under the ticker SKHY. Samsung remains the hardest of the three to own directly.

Two years ago, nobody wanted to own a memory chip stock. It was a boom-bust commodity business with thin margins and a reputation as the most boring corner of semiconductors. Then AI data centers started buying up a very specific kind of memory as fast as anyone could manufacture it, and the three companies that supply it turned into some of the most valuable chip businesses on the planet.

What HBM actually is

High bandwidth memory, or HBM, gets its name from the problem it solves rather than how it is built. Ordinary memory chips sit flat on a circuit board some distance from the processor, exchanging data through a connection that is narrow by comparison. HBM manufacturers instead stack eight or twelve memory dies directly on top of one another, punch thousands of microscopic vertical connections through that stack, and mount the whole assembly on the same piece of silicon as the processor itself. The distance data has to travel drops from centimeters to fractions of a millimeter.

That distance is the entire point, and the numbers behind it are the real story. A conventional memory module connects to a processor through a 64-bit-wide data path. A single HBM stack connects through a 1,024-bit-wide one, sixteen times as many lanes carrying data at once. Manufacturers are not making memory faster in the traditional sense. They are opening far more lanes for data to travel through simultaneously.

Why AI cannot run without it

Modern AI models are not small. A large model's parameters, the numbers that encode everything it has learned, can run into the hundreds of billions. All of them have to pass through the processor repeatedly, both while training and while answering a single prompt. A chip capable of trillions of operations per second gains nothing if it spends half its time waiting for those parameters to show up. That wait, not raw processing power, is the actual constraint on AI hardware today. HBM is the fix, which is why every flagship AI accelerator, including Nvidia's, now ships with several stacks of it soldered onto the same package as the chip.

That dependency is also what turned memory into a structural story instead of a cyclical one. A single AI accelerator can carry six or eight HBM stacks, and data centers are buying those accelerators by the hundreds of thousands. Multiply that out and a handful of AI customers can absorb more HBM capacity than the entire industry used to produce in a year. Suppliers reportedly had commitments locked in for essentially all of their 2026 output before 2026 even started.

The only three companies that make it

HBM is one of the most concentrated markets in all of tech, and the gap between the three companies that make it is enormous.

SK Hynix got there first, by winning the early contracts to supply Nvidia and defending that lead through every HBM generation since. That head start is now worth a reported 62 percent of the entire market, as of the second quarter of 2026. The stock reflects it: up roughly 280 percent in 2026 on the Korea Exchange, and its Nasdaq debut under the ticker SKHY is set to be the largest ADR offering ever.

A distant second, at a reported 21 percent, is Micron (MU), and the more interesting number is how it got there. It passed Samsung for that spot earlier this year, a shakeup nobody would have predicted two years ago, back when Samsung was still considered the safer name in memory. Shares rose about 304 percent in the first half of 2026 and briefly touched $1,255 in late June, a fixture of every chip-sector swing since. New fabs in Idaho and New York, funded partly through CHIPS Act money, are meant to grow its footprint on US soil.

Then there is Samsung, whose reported 17 percent looks almost like an afterthought next to the other two, which is strange for a company that still dominates conventional memory overall. It fell behind specifically on HBM quality certification for the newest AI chips and has been fighting to win back allocation ever since. The next round of that fight is HBM4, the coming generation, where per-stack pricing is reportedly running well above the current one.

How to actually invest in the HBM trade

Of the three, Micron takes the least effort. It already trades on the Nasdaq like any other US stock, and we broke down its numbers in our guide to reading an earnings report, using its June quarter as the worked example.

SK Hynix used to be the hard one, since owning it meant access to the Korean market that most US brokerages simply do not offer. The SKHY listing changes that math, putting the actual HBM market leader inside an ordinary US brokerage account for the first time.

Samsung is the one still stuck outside. American investors reach it mainly through foreign listings or funds that hold it directly, since no US-listed shares exist yet.

There are also sideways routes into the same story. Companies that build the tools and materials for advanced packaging benefit from every new HBM generation, and the broader memory complex, including SanDisk (SNDK) and Western Digital (WDC) on the storage side, has traded in sympathy with the HBM names all year, as this weekend's Hyperliquid tape showed again.

The risks, in plain terms

Memory has burned investors before. It is historically one of the most boom-and-bust businesses in tech, because when prices rise, every producer adds capacity at once, and the resulting glut crushes prices for years. The bet behind today's valuations is that AI demand broke that cycle for good. Maybe it did. Nobody has proven it yet.

The volatility is not theoretical either. Micron fell 5.6 percent in a single day during the July chip selloff. SK Hynix dropped 14.57 percent in one session on the Kospi before bouncing double digits the next day. Famed short seller Michael Burry disclosed a short against Micron near $1,052, arguing the AI hardware trade is priced for perfection. He may be wrong. The point is that serious people are on both sides of this trade, and the stocks move like it.

The bottom line

HBM turned memory from a commodity business into a chokepoint. Three companies control the supply of a component that every AI data center needs and cannot substitute, and their order books are full into next year. That is a genuinely rare market position. It also sits on top of the most cyclical foundation in semiconductors, priced after one of the great rallies of the decade. Understand both halves of that sentence before buying any of these names.

This is not investment advice. Prices and market shares reflect reporting as of early July 2026 and will move. Do your own research before making any investment decision.