Key points

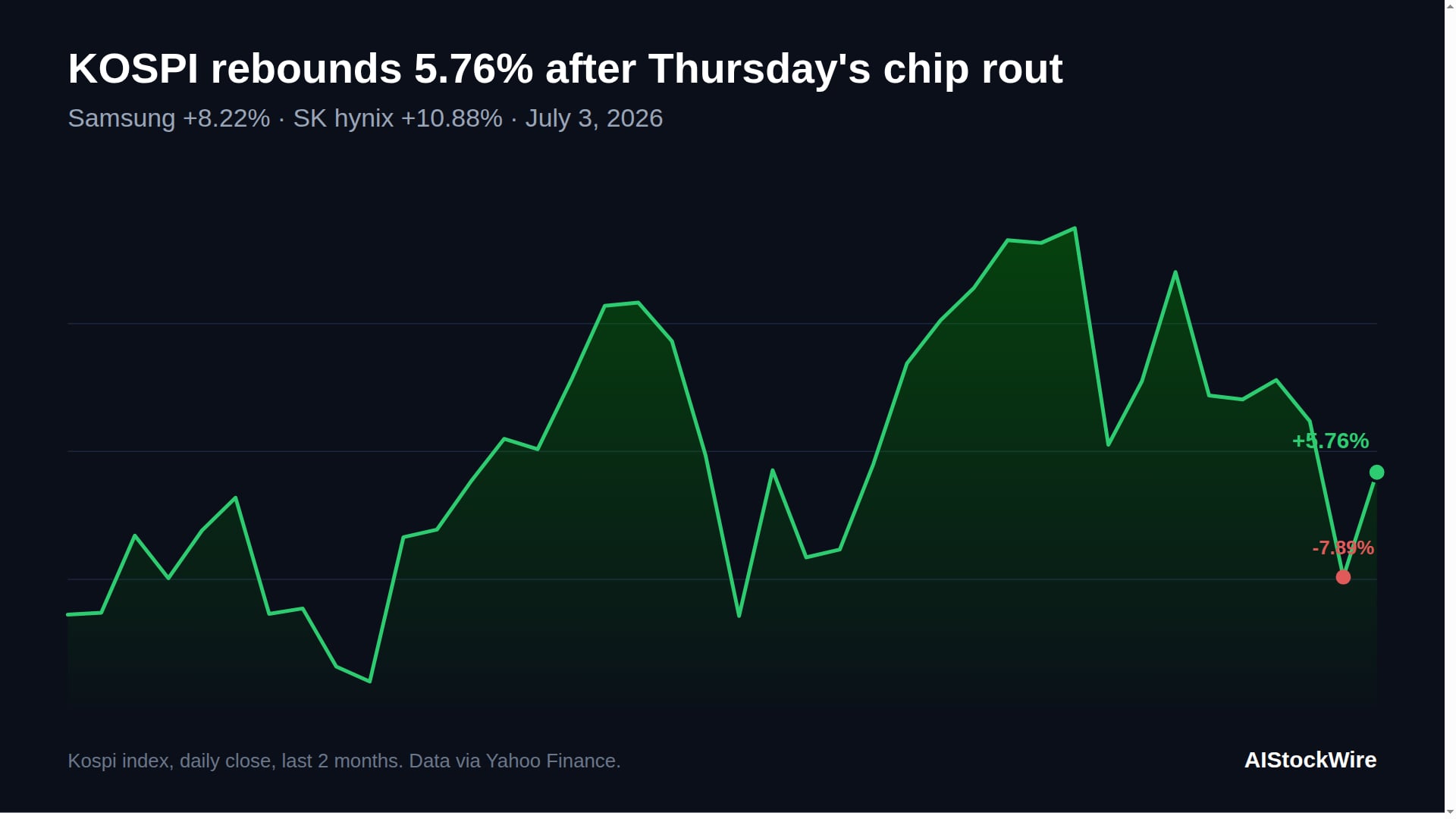

- South Korea's Kospi fell 7.89% to 7,648.09 on Thursday, then reversed to close Friday up 5.76% at 8,088.34, triggering a buy-side sidecar as automated buying kicked in.

- Samsung Electronics (+8.22%) and SK hynix (+10.88%) led the rebound, a day after tumbling 9.06% and 14.57%.

- The same down-then-up pattern showed up in China and Japan: the Shanghai Composite fell 2.03% Thursday then added 0.4% Friday, Hong Kong's Hang Seng rose 1.3%, and Japan's Nikkei 225 gained 1.5%.

- Nasdaq 100 futures are echoing the rebound, up about 1.2% Friday morning to near 29,913 from Thursday's 29,556 settlement, in a holiday-shortened session; S&P 500 futures are up a milder 0.3% and Dow futures are roughly flat.

- Zoom out and the week was still a loser for Korean chips: the Kospi closed Monday at 8,394.65 and finished Friday at 8,088.34, down about 3.65% for the week even with the rebound included. Still, ending on two sharp up days beats closing out a rough week on a fresh red candle.

Korea's stock market spent the week acting like a seismograph. The Kospi dropped 7.89% on Thursday to 7,648.09 as a fresh wave of chip-stock selling swept in from Wall Street, then reversed completely on Friday, sliding to an intraday low near 7,300 before rallying to close at 8,088.34, up 5.76% on the day. Samsung Electronics and SK hynix, which together make up more than half of the Kospi's total market value, did almost all of the work in both directions.

The same up-and-down pattern showed up across the rest of Asia, and it lines up with the setup going into the long US holiday weekend. Wall Street closed Thursday with the Dow at a record high, even as chip stocks kept sliding, and US cash markets are closed today for Independence Day, though futures are trading through midday in a holiday-shortened session.

Samsung and SK hynix do the heavy lifting

Samsung Electronics closed Friday at 309,500 won, up 8.22%, a day after falling 9.06% to 286,000 won. SK hynix moved even harder: it jumped 10.88% to 2,425,000 won, clawing back a chunk of Thursday's 14.57% drop. The two stocks are the reason the Kospi itself swung so violently, since Samsung and SK hynix alone account for more than half of the index's total weight.

The rebound was sharp enough to trigger what Korea's exchange calls a buy-side sidecar. When the Kospi rises more than 4% from the prior close, the Korea Exchange automatically pauses program trading (algorithmic and basket orders) for five minutes, while regular investors keep trading as normal. It is the mirror image of a sell-side sidecar, and it exists to slow down index moves that automated buying or selling is amplifying, rather than moves driven by fresh news.

This is the same trade that hit Micron (MU) in the United States earlier this week, when Micron slipped back under $1,000 as the Korean selloff spread overnight. Chips had already logged their third-worst day of 2026 just two sessions before Thursday's rout in Korea, so Friday's bounce looks like traders deciding the selling had gone too far, not proof that the underlying worry, whether AI computing capacity is being built faster than demand can absorb it, has actually been resolved.

China and Japan followed the same script

This was not just a Korea story. The Shanghai Composite fell 2.03% Thursday to 4,029, snapping a three-day winning streak, then added 0.4% on Friday. Hong Kong's Hang Seng gained 1.3% Friday and the mainland's CSI 300 rose 0.6%. Japan's Nikkei 225 climbed 1.5% as Japanese chip and memory names bounced alongside their Korean peers.

Behind the bounce were three things happening at once: bargain hunters stepping into semiconductor stocks they judged had fallen too far, President Trump saying tensions with Iran had eased and that Tehran was open to resuming talks, which knocked oil prices down and helped risk appetite broadly, and a soft US jobs report. June payrolls grew by just 57,000, roughly half of what economists expected, and the unemployment rate ticked down to 4.2%. Weak hiring numbers like that keep alive the case for the Federal Reserve to cut rates later in 2026, which is generally read as good news for stocks.

What it means for Monday

Wall Street's last full trading session before the holiday, Thursday, was itself a split picture. The Dow Jones Industrial Average closed at a fresh record, up more than 1.1%, on the back of the soft jobs report and rate-cut hopes. The Nasdaq fell about 0.8% for a second straight day as chip stocks kept sliding: Micron dropped roughly 7%, Applied Materials fell 7.4%, and AMD lost 4.3%. So the backdrop heading into the long weekend is a market comfortable with rate-cut optimism and record highs in blue-chip names, but still nervous about how far AI chip valuations can run.

There is a live data point that lines up with Asia's move: US index futures are trading right now in a holiday-shortened Globex session that runs from Thursday evening to Friday midday Central time, and they are pointing higher. Nasdaq 100 futures were near 29,913 Friday morning, up about 1.2% from Thursday's 29,556 settlement. S&P 500 futures were more modestly higher, near 7,553 versus Thursday's 7,528 close, up about 0.3%, while Dow futures sat roughly flat around 53,121. The bigger move in Nasdaq futures fits a tech-led bounce, the same story playing out in Samsung and SK hynix. It is a real, tradable move, but it happened in a lower-volume holiday session rather than a normal premarket, so treat it as a lean, not a lock.

None of that guarantees anything for Monday. Friday's Asia rebound, the tech-led futures bounce, and Thursday's Dow record are all constructive signals, and markets do tend to read a broad, multi-market move like this as a sign that a selloff has found a floor. But Samsung and SK hynix are still down sharply for the week even after Friday's gains, and this is the same chip sector that has whipsawed more than once in the past month. Treat Friday's move as encouraging, not as a forecast.

A rough week, but a strong finish

Zoom out from Friday alone and the week itself was still a net loser for Korean chip stocks. The Kospi closed Monday at 8,394.65 and finished Friday at 8,088.34, a decline of about 3.65% even with the rebound baked in. Samsung and SK hynix are down for the week on the same basis, and this was the week that also delivered a record-setting chip rout and a fresh scare over AI spending.

That context matters, but so does the order events happened in. A week that includes a brutal selloff and then closes with two straight days of sharp buying, culminating in a buy-side sidecar, reads differently to markets than one that ends on a fresh low. It is a genuinely better setup heading into Monday than Thursday's rout alone would have been, even if it is not proof the chip selloff is fully behind the market.