Key points

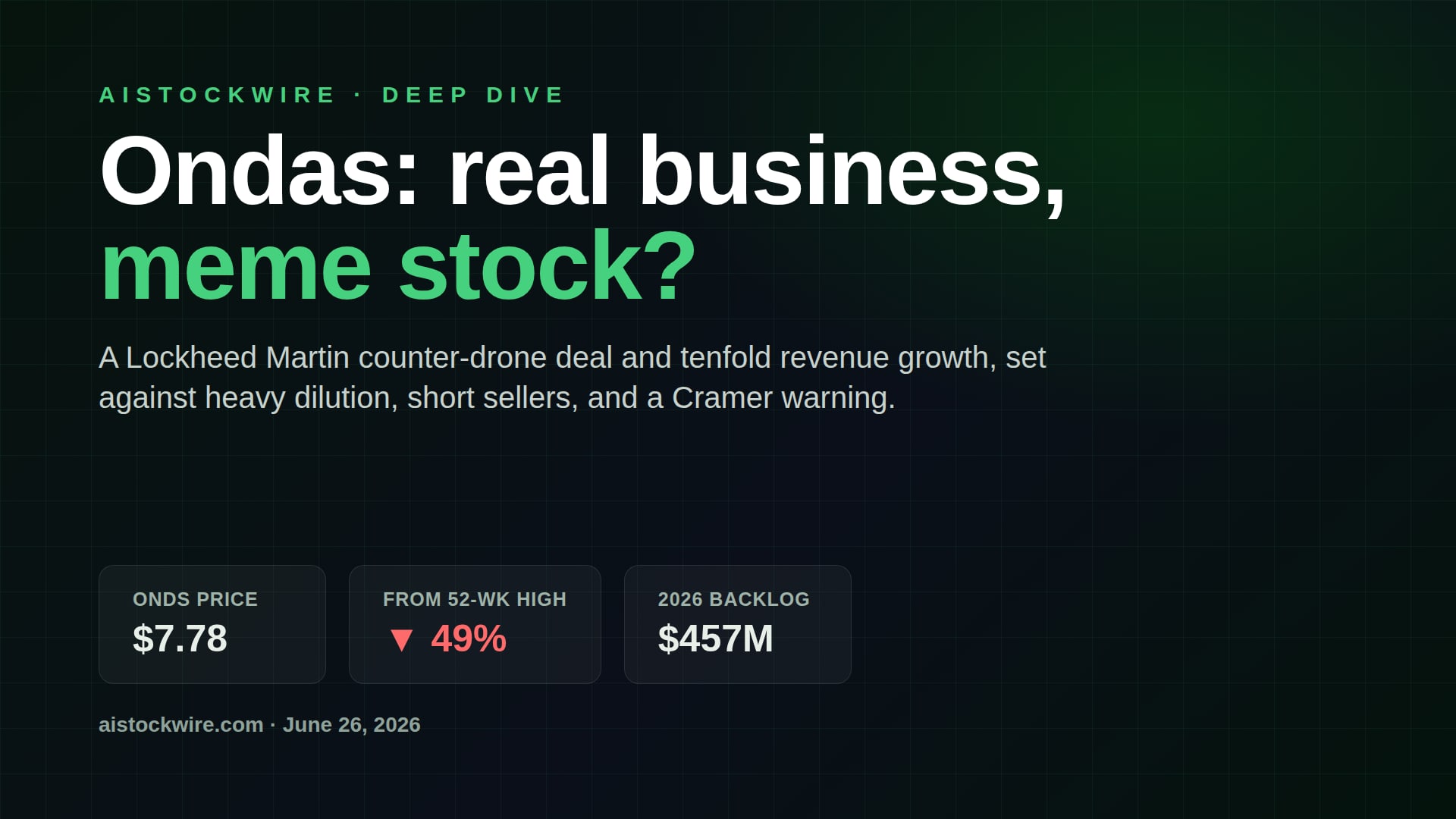

- Ondas (ONDS) trades around $7.70 in late June 2026, roughly 49% below its 52-week high of $15.28 and down from the mid-$13s a month earlier.

- Its Sentrycs unit will integrate counter-drone technology into Lockheed Martin's (LMT) Sanctum C-UAS platform, announced June 23, 2026.

- Revenue jumped about tenfold to $50.1 million in the first quarter of 2026, and the company raised full-year guidance to at least $390 million with a $457 million backlog.

- Ondas raised about $1 billion in January and has made at least six acquisitions in 2026, including the defense prime Mistral, lifting shares outstanding to about 508 million.

- Short interest sits near 30% of the float, the CEO sold about $31.9 million of stock on June 1, and Jim Cramer called ONDS a meme stock on June 9.

Ondas Holdings (ONDS) is two stories at once, and they point in opposite directions. The business is growing about as fast as a small company can grow: revenue up tenfold, a marquee deal with Lockheed Martin (LMT), and a backlog that did not exist a year ago. The stock, meanwhile, has been cut roughly in half from its high, sliding from the mid-$13s in late May to around $7.70, including an 8% drop on June 26. Both of those things are true at the same time, and the gap between them is the whole story.

Here is the full picture: what Ondas actually does, the deals it has signed, the money it has raised, who is shorting it, why the CEO is selling, why Jim Cramer called it a meme stock, and where the price sits now.

What Ondas actually is

Ondas runs two businesses. The original one is Ondas Networks, which sells private wireless gear for railroads and other critical industries. The one driving the stock is Ondas Autonomous Systems, or OAS, a fast-assembled group of drone, counter-drone, robotics and defense companies. Through more than a dozen acquired businesses, including American Robotics, Airobotics, Sentrycs, Roboteam, Apeiro Motion, Omnisys and the U.S. defense prime Mistral, OAS now sells the Optimus drone-in-a-box for automated security, the Iron Drone Raider that intercepts hostile drones, Cyber-over-RF technology that takes control of rogue drones without jamming, tactical ground robots, stratospheric sensing and the mission software that ties it together. In plain terms, Ondas has bought its way into being a one-stop shop for drones, counter-drones and defense autonomy, and the Mistral deal in April even made it a direct U.S. defense prime contractor.

The Lockheed Martin deal

On June 23, 2026, Ondas said its Sentrycs unit would integrate its Cyber-over-RF counter-drone technology into Sanctum, the counter-UAS platform built by Lockheed Martin (LMT). Sentrycs works at the communication-protocol layer: instead of jamming a drone or shooting it down, it detects the drone, takes control of it, and guides it to a safe landing without interfering with nearby communications. Lockheed's Sanctum is the bigger system that fuses sensors, AI and command-and-control to handle complex threats, including drone swarms. Getting Sentrycs inside a Lockheed platform is exactly the kind of validation a small defense company wants.

And yet the stock dipped on the news. The reason is worth understanding: the announcement was a collaboration, not a purchase order. No dollar value was attached, and integration deals can take a long time to turn into revenue. For a stock priced for fast growth, a headline without a number is not enough.

An acquisition spree

Most of the story is the buying. Ondas built the core of OAS over the past few years by acquiring American Robotics and Airobotics, the companies behind the Optimus and Iron Drone products, then added the counter-drone firm Sentrycs and the ground-robotics makers Roboteam and Apeiro Motion through 2025. Apeiro, an Israeli company bought for about $12 million, brought quadruped robots, unmanned ground vehicles and fiber-optic spools that let drones fly on a jam-proof tether. Then 2026 turned into a spree. By the time Ondas agreed to buy Cyberhawk on June 18, one outlet counted it as the company's sixth acquisition of the year.

| Company | What it adds | Terms | When |

|---|---|---|---|

| Mistral | U.S. defense prime status; Army and Special Operations contract access; about $264M of backlog | About $175M, mostly stock | April 2026 |

| INDO Earth Moving | Military heavy-engineering vehicles tied to a $140M supply tender | About $5.7M cash plus stock and up to $140M in earn-outs | March 2026 |

| World View | Stratospheric ISR using long-endurance high-altitude sensing | Undisclosed | 2026 |

| 4M Defense | AI land intelligence for demining and border security | Undisclosed | 2026 |

| Omnisys | AI "Battle Resource Optimization" defense planning software | About $196.6M in stock | May 2026 |

| Cyberhawk | Drone-based inspection and infrastructure AI; 40 countries, 300-plus customers | About $125M, roughly 95% cash | Announced June 2026, closing Q3 |

The strategy is clear: become a single autonomous-systems and defense platform spanning air, ground, the stratosphere and software. The Mistral deal is the most important of the group, because it turned Ondas into a direct U.S. defense prime with access to Army and Special Operations contract vehicles and a program portfolio the company values at more than $1 billion. The question is what all this buying costs shareholders, which brings us to the other side of the ledger.

The business numbers are real

This is not a shell with a story. In the first quarter of 2026, Ondas reported revenue of $50.1 million, about ten times the prior year and more than 25% above the high end of its own guidance, led by counter-drone and defense products. It raised full-year 2026 revenue guidance to at least $390 million, which would be roughly a 670% jump. Its pro forma backlog reached $457 million as of the end of the first quarter, up from $68.3 million at the end of 2025, with much of that jump coming from Mistral's roughly $264 million in contracted programs. The product companies turned adjusted-EBITDA positive about six months ahead of plan, and Ondas finished the quarter with about $1.48 billion in cash and investments. It also said it booked more than $40 million of new defense orders in June and more than $150 million of order activity in the second quarter.

Now the other side: dilution

That $1.48 billion in cash did not come from selling drones. In January 2026, Ondas priced a roughly $1 billion stock-and-warrant offering, selling shares and pre-funded warrants at $16.45 per unit, with seven-year warrants exercisable at $28.00. The raise added about 60 million share equivalents on its own. On top of that, several acquisitions were paid largely in stock, including the roughly $196.6 million Omnisys deal and the $175 million Mistral merger, and Ondas has been registering those shares for resale. From May 21 to June 22, it issued about 16.8 million shares tied to Omnisys alone.

Add it up and Ondas now has about 508 million shares outstanding, a number that has ballooned as the company funded its growth by printing stock. Every new share is a real claim on the business, and the steady drip of resale registrations creates what traders call an overhang: the market knows more shares are coming, so buyers wait and sellers move first. That is a big part of why good news keeps getting sold.

Insider selling and short interest

Two more weights sit on the stock. First, insiders are selling. Chairman and CEO Eric Brock sold about 2.38 million shares for roughly $31.9 million on June 1, 2026, and additional Rule 144 filings have pointed to more stock coming to market. Insider sales are not always a red flag, but a large one during a volatile stretch does not help confidence.

Second, the bears are out in force. Short interest has climbed through 2026, from around 21% of the float late last year to somewhere around 30% to 35% by late spring, with well over 150 million shares sold short at the peak. The catch for squeeze hunters is that ONDS trades enormous volume, often tens of millions of shares a day, so the days-to-cover figure is low. A high short interest can fuel sharp rallies, but with this much liquidity, a classic lasting squeeze is harder to engineer than the float number alone suggests.

Cramer's meme-stock call

On June 9, 2026, during the lightning round on Mad Money, Jim Cramer was asked about Ondas and did not hedge. "It's just a meme stock," he said. "It's about the autonomous system meme, and I can't get behind a meme stock. This market's too horrible. A meme stock could rip your lungs out." It was a blunt way to make a real point: when a stock moves on theme and momentum more than on numbers, it can fall as fast as it rose. ONDS proved his point in miniature when it spiked about 20% intraday on May 28 to nearly $13 on light news, then slid back into the $7s over the following weeks.

So what is it worth?

This is where the two stories collide. On trailing revenue of about $97 million, Ondas carries a market value near $3.9 billion, or roughly 40 times sales. Measured against the $390 million the company expects this year, it is closer to 10 times forward sales, which is still a rich multiple for a hardware-heavy defense business. Wall Street analysts are mostly bullish, with a Strong Buy consensus and an average price target around $20, more than double the current price, and Needham carrying a $23 target. The market, so far in June, has voted the other way.

| Metric | Value |

|---|---|

| Price (late June 2026) | Around $7.70, after an 8% drop on June 26 |

| 52-week range | $1.53 to $15.28 |

| From the high | Down about 49% |

| Market cap | About $3.9 billion |

| Shares outstanding | About 508 million |

| Revenue (trailing 12 months) | About $97 million |

| 2026 revenue guidance | At least $390 million |

| Backlog (pro forma) | About $457 million |

| Cash and investments | About $1.48 billion |

| Short interest | Roughly 30% of float (recent) |

| Beta | 2.62 |

Figures as of late June 2026.

Bottom line

Ondas is the rare meme stock with a real, fast-growing business attached. The drone and counter-drone demand is genuine, the Lockheed Martin (LMT) integration is a real credential, the Mistral deal made it an actual U.S. defense prime, the backlog is real, and the company is sitting on more than a billion dollars in cash. But the stock is not trading on any of that right now. It is trading on supply and sentiment: a flood of new shares from a $1 billion raise and a string of stock-funded deals, resale overhangs, insider selling, heavy short interest, and a valuation that leaves no room for a miss. Cramer's line was crude, but the mechanism he described is the one driving the price. For now, the business is winning and the stock is losing, and which one matters more depends entirely on your time horizon and your stomach for volatility.

For more on how richly valued AI and defense names have traded this year, see our look at whether the AI trade has gotten ahead of itself and our piece on how the market is grading AI pivots one at a time. You can also track filings for Ondas (ONDS) and Lockheed Martin (LMT).

This article is for general informational purposes only and is not investment advice. Ondas is a highly volatile small-cap stock, and the numbers here can change quickly. Always do your own research and consider speaking with a licensed financial professional before making any investment decision.