Key points

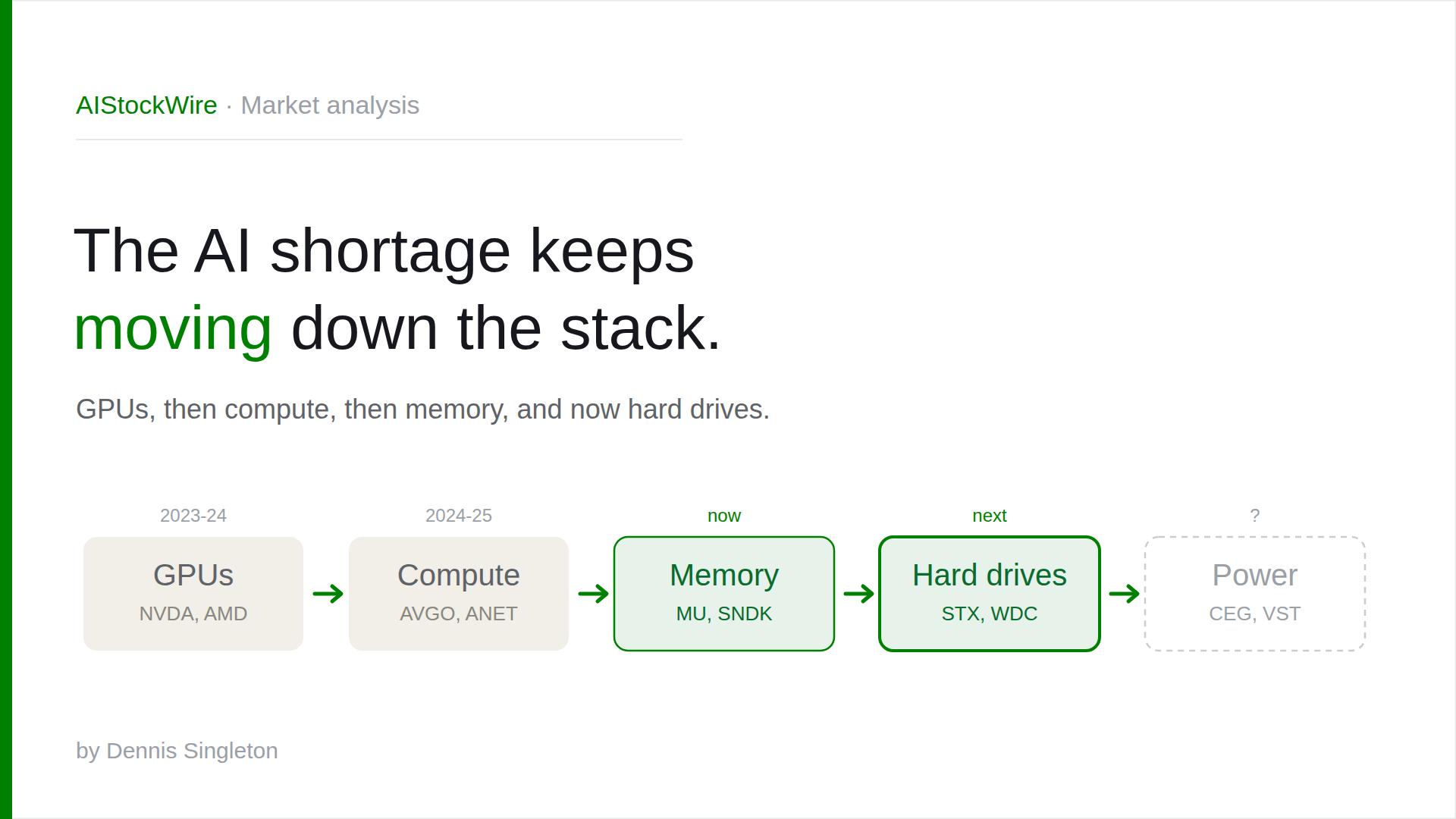

- The AI shortage rotates down the stack: GPUs, then compute, then memory, and now hard drives.

- Nvidia (NVDA) is up about 4x since 2023; Micron (MU) about 2.8x and Sandisk (SNDK) about 3.7x in 2026.

- Hard drives are next: Seagate (STX) and Western Digital (WDC) have more than doubled in 2026.

- Power (Constellation CEG, Vistra VST, Vertiv VRT) looks like the leg after that.

One pattern keeps repeating in the AI trade, and once you see it, you cannot unsee it. A shortage shows up in one layer of the supply chain. Prices spike, the layer sells out, and the stocks that own that layer re-rate, often two to four times over. Then the bottleneck moves one step down the stack and the whole thing happens again. It started with GPUs. It ran through the rest of the compute rack. Right now it is memory. And the next leg, hard drives, is already lighting up.

Here is the cycle, stage by stage, with what each shortage did to the stocks, and where it looks to be heading next.

The pattern

The mechanics are the same every time. AI demand for some component grows faster than the few companies that make it can add supply. Lead times stretch, the product sells out, and because buyers have nowhere else to go, prices rise. For a maker, that is the dream: a commodity business suddenly gets pricing power, margins jump, and the stock gets repriced as a growth story instead of a cyclical one. Then the constraint relocates to the next thing the buildout needs, and the market goes looking for the next sold-out supplier. Our AI stock map lays out the full stack this rotation travels through.

Stage 1: GPUs (2023 to 2024)

This is where the phrase "AI shortage" entered the language. Training large models needed Nvidia (NVDA) accelerators, lead times stretched toward a year, and the company could sell every chip it made. Nvidia is up roughly four times from the start of 2023, and far more than that measured from its late-2022 low. AMD (AMD) rode the same wave as the credible second source. GPUs were the first bottleneck, and they minted the first wave of AI winners.

Stage 2: The rest of the compute rack (2024 to 2025)

A pile of GPUs does nothing on its own. They need server CPUs to run them, custom chips to escape Nvidia's pricing, and a network fast enough to tie thousands of them into one machine. So the shortage and the spending moved outward. The CPU makers came back to life: AMD (AMD) has more than doubled in 2026, and even Intel (INTC), which had collapsed to around $19 in early 2025, has surged back above $125, up roughly 2.8 times in 2026 alone on renewed hope for its data-center chips and foundry. Around them, Broadcom (AVGO) custom AI silicon and Arista (ANET) switches each rose about four times from early 2023. Same pattern, one layer over: the parts around the GPU became the scarce thing.

Stage 3: Memory (2026, happening now)

The current leg, and the cleanest example yet. A GPU is useless without memory fast enough to feed it, and that memory is sold out. Micron (MU) just reported a record quarter and is up nearly three times in 2026. Sandisk (SNDK), the highest-leverage flash play, has risen even more, and SK Hynix and Western Digital are part of the same move. We covered the memory leg in detail in why Sandisk ripped on Micron's blowout. High-bandwidth memory, DRAM, and NAND are all running tight, prices are climbing, and the makers are printing the kind of margins that only show up when a product is genuinely scarce.

Stage 4: Hard drives (starting right now)

This is the question worth asking, and the answer is that it is already underway. All the data AI generates and trains on has to be stored somewhere, and at scale the cheapest place to keep it is a hard drive. The setup here is almost a caricature of the pattern.

- Only three makers are left: Seagate (STX), Western Digital (WDC), and Toshiba.

- Demand is growing about 40% to 50% a year while supply expands only 30% to 35%, a gap that does not close quickly.

- Western Digital sold out its entire 2026 hard-drive production before the year was half over. Seagate's high-capacity capacity is committed through 2027. Morgan Stanley thinks the shortage could last to 2028.

- Nearline drive prices sit around $15 per terabyte and makers expect to push them toward $25 to $30 over the next few years.

- Western Digital now earns about 89% of its revenue from hyperscaler AI cloud customers, versus a sliver from consumers.

The market has noticed. Seagate is up more than two times in 2026 and Western Digital nearly two and a half times, and both have hit record highs. Storage is no longer a sleepy commodity business. It is the freshest leg of the AI shortage.

The price moves, side by side

The same story told in numbers. These are rough multiples, not precise entry points, but they show how consistently the pattern has paid.

| Stage | The shortage | Key stocks | The run-up |

|---|---|---|---|

| 1 | GPUs (2023-24) | Nvidia (NVDA), AMD | NVDA about 4x since Jan 2023 |

| 2 | Compute and networking | AMD, Intel (INTC), Broadcom (AVGO), Arista (ANET) | INTC and AMD about 2.8x in 2026; AVGO, ANET about 4x |

| 3 | Memory (now) | Micron (MU), Sandisk (SNDK), SK Hynix | MU about 2.8x, SNDK about 3.7x in 2026 |

| 4 | Hard drives (next) | Seagate (STX), Western Digital (WDC) | STX about 2.3x, WDC about 2.4x in 2026 |

So what is next?

If the bottleneck always relocates, the useful question is where it goes after storage. The layer with the most runway left is power. AI data centers are increasingly limited not by chips but by electricity, which is pulling nuclear and gas producers like Constellation (CEG) and Vistra (VST), and power and cooling suppliers like Vertiv (VRT), into the same trade. We walked through the power leg in AI's power problem could be nuclear's big break. Cooling is a close cousin: as racks get denser, liquid cooling becomes its own shortage story.

One honest caveat. Each leg carries more risk the later it runs, because more of the move is already in the price by the time the headlines arrive. And every one of these is a cyclical business at heart. The same scarcity that sends them up two or three times can reverse when capacity finally catches demand, and these stocks fall as fast as they rose. The pattern is real, but it is not a guarantee.

How to actually use this

The lesson is not to chase whatever just ran. By the time a layer is on the front page, much of the re-rating has happened. The edge is in spotting the next "sold out" signal early, the layer where demand is quietly outrunning supply and pricing is about to inflect. Watch order books, lead times, and capacity commitments, not just stock charts. That is where the next leg of this cycle announces itself.

Bottom line

The AI shortage is not a single event, it is a rolling one. It moved from GPUs to the rest of the compute rack to memory, and it is now reaching hard drives, with power lined up behind it. Each stop has followed the same script: sold out, pricing power, re-rating. Knowing the script does not tell you exactly when each leg turns, but it tells you where to look.

Sources

- 24/7 Wall St., Seagate and Western Digital: AI storage demand is now showing up in pricing power

- TradingKey, Western Digital and Seagate hit record highs as Morgan Stanley flags HDD shortage through 2028

- Trefis, Seagate is sold out through 2027 as AI reshapes hard-drive demand

This article is for general informational purposes only and is not investment advice. Prices and multiples are approximate and as of late June 2026, and will change. Always do your own research and consider speaking with a licensed financial professional before making any investment decision.