Key points

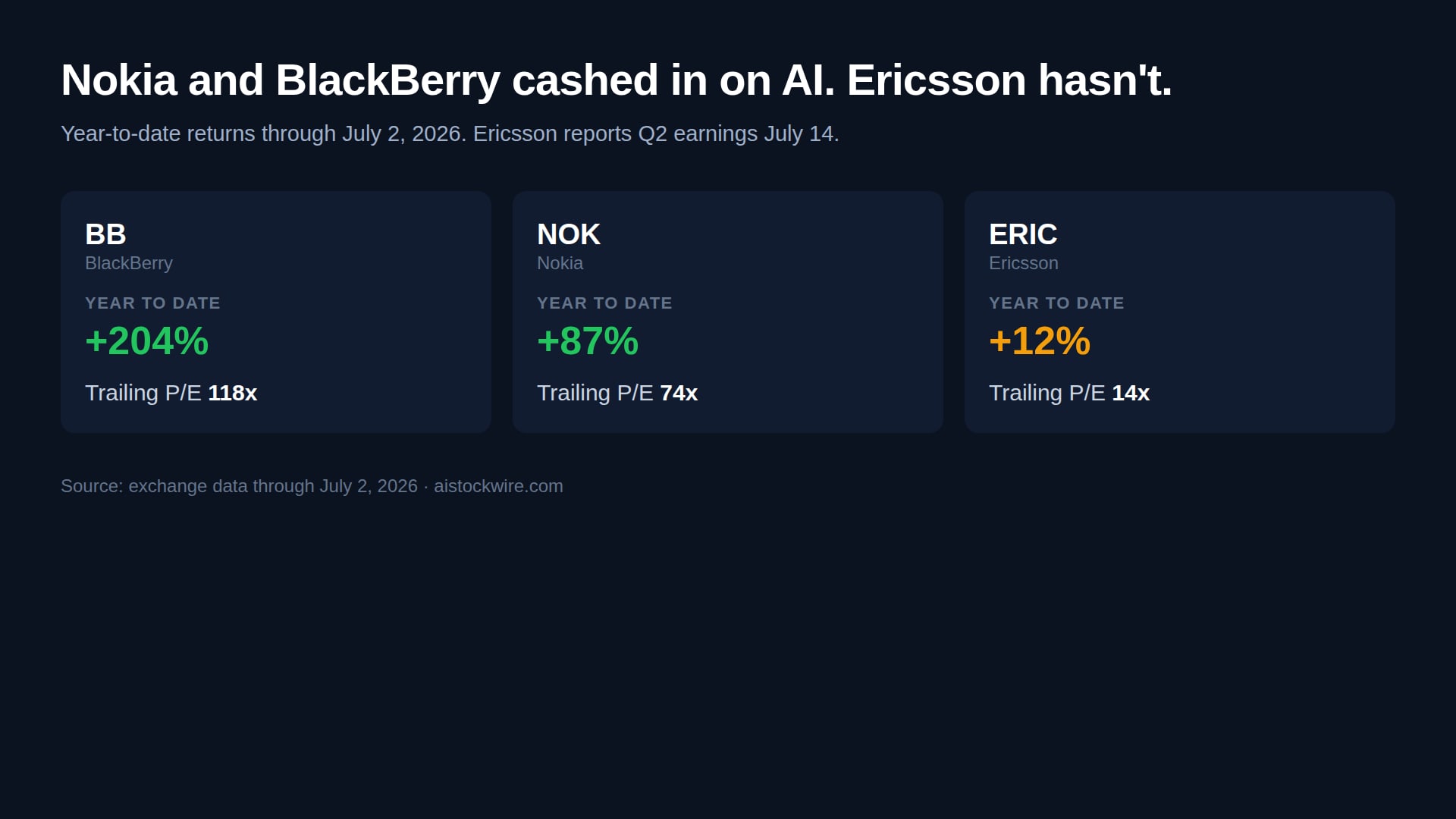

- Nokia (NOK) is up about 87% and BlackBerry (BB) about 204% this year after real AI pivots. Ericsson (ERIC) is up about 12%.

- Nokia took a $1 billion Nvidia investment and became a preferred AI data-center vendor. Ericsson chose to build AI-RAN on its own silicon with Intel instead, and avoided a deep Nvidia tie-up.

- In Q1 2026, rising AI-driven chip costs actually hurt Ericsson's margins. That is the opposite of what happened at Nokia and BlackBerry.

- Ericsson reports Q2 earnings July 14. Consensus EPS is $0.13, the same number it missed badly last quarter ($0.03 actual). Watch North America sales and the 49 to 51 percent gross margin guide.

We have written twice now about old phone brands turning into AI stocks. Nokia (NOK) took a billion-dollar bet from Nvidia and never looked back, a story we covered in our look at the whole group and one David has written about holding personally. BlackBerry (BB) turned its old car software into a physical AI story and popped over 20% on the earnings that proved it. Both times, that first piece mentioned a third name in passing: Ericsson (ERIC), Nokia's old rival in the same radio equipment business.

Ericsson never got its own look. It is worth one now, because the honest answer is not flattering. While Nokia and BlackBerry went all in on AI and the market rewarded them for it, Ericsson took a different road, and so far it has nothing to show for it. With earnings landing July 14, this is the moment to lay out why.

What Nokia and BlackBerry actually did

Nokia stopped selling network gear the old way and let Nvidia in. In late 2025, Nvidia put roughly $1 billion into Nokia and the two started building AI-RAN software together, technology that uses AI chips to run wireless networks. Nokia also landed a role as a preferred vendor for Nscale, an AI data-center buildout. The market noticed. Nokia is up about 87% year to date, and even after giving back a chunk of its June highs, it still trades at a rich 74 times trailing earnings.

BlackBerry took a quieter path to the same place. Its QNX software, the operating system that runs safety-critical computers, is now the brains behind what people call physical AI, robots and self-driving cars that cannot afford to crash. That business grew 26% last quarter, and BlackBerry posted its first positive cash flow in a fiscal first quarter in nine years. The stock is up roughly 204% this year and trades at 118 times trailing earnings, an eye-watering multiple that only makes sense if you believe the AI story is just getting started.

Ericsson bet against needing Nvidia

Ericsson looked at the same AI-RAN opportunity and chose to go it alone. Instead of leaning on Nvidia's chips the way Nokia did, Ericsson is building its AI-RAN products on its own custom silicon, developed with Intel. There is a small T-Mobile pilot running on Nvidia's platform and a joint AI-RAN research center, but nothing close to a billion-dollar investment or a marquee data-center vendor role.

That strategic choice shows up directly in the numbers. In Ericsson's first quarter of 2026, management said rising semiconductor costs, pushed up by AI demand elsewhere in the industry, were part of why margins fell. For Nokia and BlackBerry, AI has been a reason to buy the stock. For Ericsson, so far, it has mostly been a reason costs went up.

The gap in one table

| Stock | Year to date | Trailing P/E |

|---|---|---|

| BlackBerry (BB) | +204% | 118x |

| Nokia (NOK) | +87% | 74x |

| Ericsson (ERIC) | +12% | 14x |

Those trailing multiples on Nokia and BlackBerry are not typical value-stock numbers. They are growth-stock numbers, the market pricing in years of AI upside that has not fully arrived yet. Ericsson, at 14 times earnings, is priced like an ordinary telecom equipment maker, because right now, that is basically what it is.

What to expect on July 14

Ericsson reports its second quarter before the market opens on July 14. The setup is tense, because the same $0.13 consensus estimate is the exact number Ericsson missed by a mile last quarter, when it posted just $0.03 against a $0.13 estimate. That miss came from a North America pullback after a big 2025 spending surge, a strong Swedish krona working against reported results, and those AI-driven chip costs eating into margin.

Three things will decide whether July 14 looks more like a relief or a repeat. First, North America sales, since that region caused most of the damage last quarter and needs to show it was a one-time pullback rather than the new normal. Second, Networks gross margin, which management has guided to 49 to 51 percent. Landing inside that range would say Q1 was noise. Missing it again would say the cost pressure is sticking around. Third, currency, since a stronger krona keeps working against Ericsson's reported numbers no matter how the underlying business performs.

If North America stabilizes and margin lands in range, expect the stock to climb back toward its June highs near $13 to $14. If North America keeps sliding or margin misses again, a retest of the $8 to $9 area is realistic, and the AI angle will not save it either way, because the market is not currently pricing Ericsson for an AI surprise.

The honest bottom line

Ericsson has a real AI-RAN business and real research partnerships. It is just not the same bet Nokia and BlackBerry made, and the market has not treated it the same way. Nokia and BlackBerry are being priced like AI growth stocks. Ericsson is being priced like the network equipment company it has always been. July 14 will mostly be a referendum on the old business, North America orders and Networks margin, not a verdict on AI. That could change if Ericsson lands a marquee AI or data-center deal of its own. Until then, its earnings will move on the same things they always have.

Sources

- Ericsson Q2 2026 earnings date and EPS estimates, and BlackBerry and Nokia fundamentals, from exchange and earnings data through July 2, 2026.

- Nvidia's investment in Nokia and the AI-RAN partnership, and Ericsson's custom-silicon strategy with Intel, via published 2026 industry coverage.

This is general market commentary and opinion, not investment advice. Prices and multiples are as of the July 2, 2026 close and will move. Markets can go down as well as up, and you can lose money. Always do your own research and consider speaking with a licensed financial professional before making any investment decision.