Key points

- A private investor who was on a group Zoom call with Ondas CEO Eric Brock says Brock told participants the company is building a platform that will reach a $20 billion market cap "and not stop there."

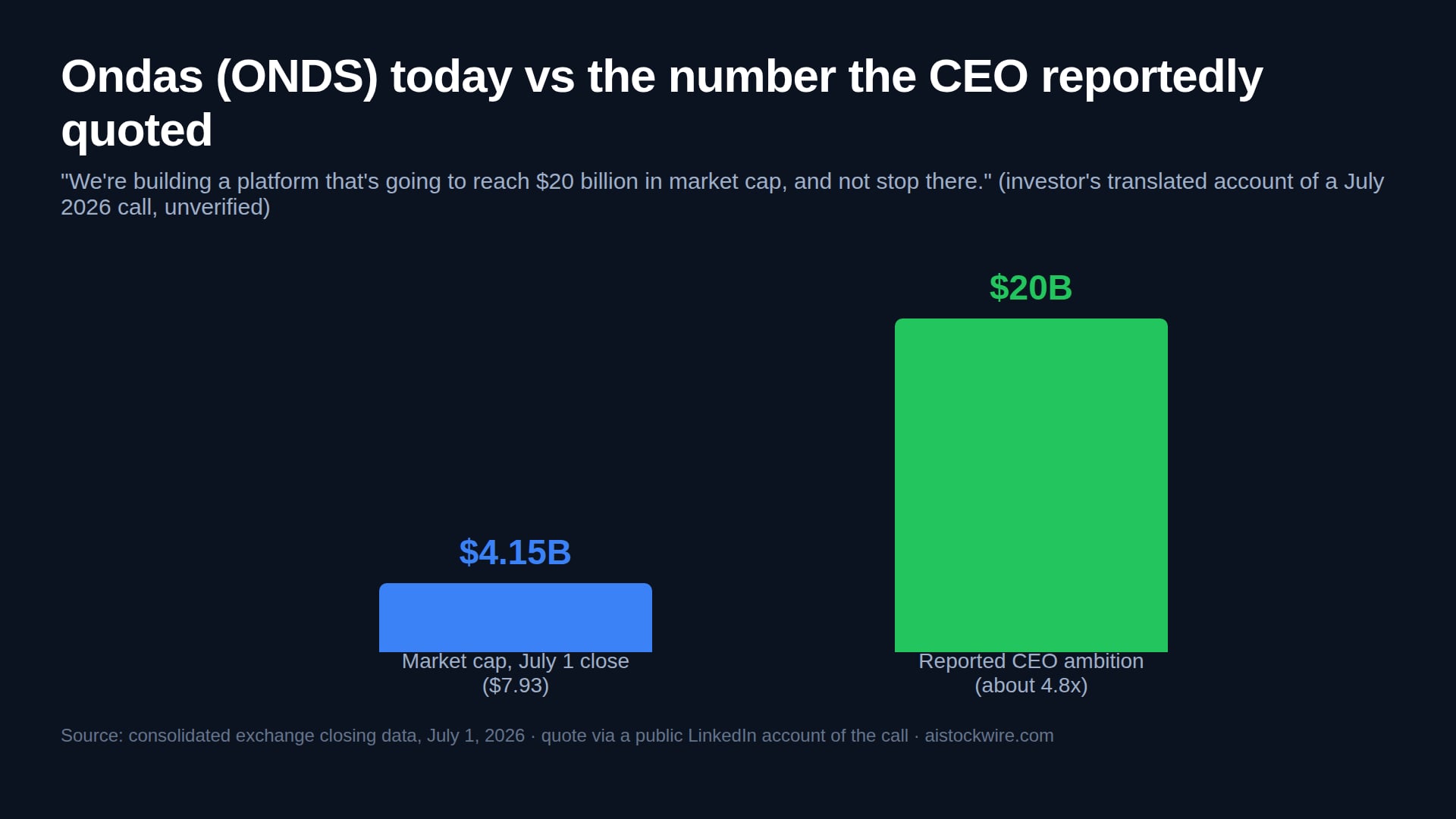

- Ondas (ONDS) closed July 1 at $7.93 with a market cap around $4.15 billion, so the reported target is roughly 4.8x today's value, or about $38 per share at the current share count.

- The business behind the talk is real: Q1 2026 revenue grew about tenfold to $50.1 million, full-year guidance is at least $390 million, and the backlog sits near $457 million.

- The caveats are real too: the quote is a secondhand, translated account, the share count keeps growing through stock-funded deals, and short interest just hit a record 167.5 million shares, about 33% of the float.

Ondas Holdings (ONDS) investors got an unusual data point this week, and it did not come from a press release. It came from LinkedIn.

What was reportedly said

David Ben Ishay, a private investor who says he has followed Ondas for years and holds a position, posted on LinkedIn about a group Zoom call he joined with CEO Eric Brock. The call ran about an hour, by his account, with Brock walking through strategy, numbers, growth engines and risks, and taking questions from analysts. Ben Ishay says he skipped the questions and simply thanked Brock for how he runs the company. He says Brock responded with a line worth writing down: "We're building a platform that's going to reach $20 billion in market cap, and not stop there."

Some honesty about sourcing before we go further. That quote is one participant's account of a call we were not on, translated from Hebrew, and we could not independently verify it. Ben Ishay disclosed his position and framed the post as personal opinion. It was not said in an SEC filing or a press release, it came with no timeline, and a market cap target is an ambition, not guidance. Treat it accordingly.

Still, it is worth taking seriously as a window into how the CEO thinks about scale. So let us do what the market does and check the number against reality.

The math on $20 billion

Ondas closed July 1 at $7.93, down 3.8 percent in a session where most of tech's hardware complex got hit. With about 523 million shares outstanding, that is a market cap around $4.15 billion. The reported target is roughly 4.8 times that. At today's share count, $20 billion works out to about $38 per share.

Hold on to that phrase, "at today's share count," because it is doing a lot of work. Ondas pays for growth with stock. It raised about $1 billion in January and has made at least six acquisitions in 2026, several funded mostly with shares. The share count was around 508 million when we profiled the company in late June and is about 523 million now. A company can grow its market cap 4.8x while the stock does something much less exciting, if enough new shares come out along the way. Market cap targets and shareholder returns are cousins, not twins.

The other yardstick is sales. Ondas has guided to at least $390 million of revenue this year. A $20 billion valuation would be about 51 times that number. Today's $4.15 billion is already about 10.6 times. For the bigger number to make sense, revenue has to keep compounding for years, which is exactly what Brock is betting the drone buildout delivers.

What is real behind the talk

The growth engine is not imaginary. First-quarter revenue rose about tenfold to $50.1 million, and the backlog sits near $457 million. In April, the Mistral deal made Ondas a direct U.S. defense prime contractor. On June 18, it agreed to buy Cyberhawk, a drone-inspection firm with customers in more than 40 countries, in a deal reported at about $125 million. And on June 23, its Sentrycs unit landed the marquee headline: integrating its counter-drone technology into Lockheed Martin's (LMT) Sanctum platform.

Materials presented on the call back the growth story up. A slide from the company deck shown to participants lists $1.4 billion in cash and short-term investments, the $457 million backlog with the World View and Mistral additions included, and a claim that Ondas reached adjusted EBITDA profitability at the product-company level six months ahead of its own forecast. Adjusted numbers deserve the usual grain of salt, but a $1.4 billion war chest is a real asset for a company still buying its growth.

That is a lot of validation for a company that was doing a tenth of this revenue a year ago. The drone sector around it is running hot, too, as we covered when the whole group rallied on June 30.

What the skeptics will say

The stock tells a rougher story than the CEO does. ONDS trades roughly half off its January high of $15.28, even though it is still up about 4.6x from its 52-week low of $1.71 last July. Both facts are true, and both matter. Short interest just hit a record: 167.5 million shares as of the latest FINRA report, about 33 percent of the float, and roughly double the 81 million shares reported in mid-January. That is a lot of professional money betting against the roll-up strategy. The curious footnote is that borrowing the stock still costs only about 3.7 percent a year, with about 250,000 shares available to borrow as of July 1. Shorts are crowded, but they are not being squeezed on borrowing fees yet. Jim Cramer called it a meme stock in June.

And Brock himself sold about $31.9 million of stock on June 2. The filing context matters here: the sale covered tax withholding on a vesting grant of 4.5 million restricted shares, and he still holds about 4.7 million shares afterward. That is a routine mechanic, not a red flag by itself. But it is fair to note that the man describing a $20 billion future was, mechanically or not, a seller in the mid-$13s a month before the stock hit $7.93.

How to read it

CEOs of acquisitive small caps talk big on investor calls. That is part of the job, and Brock has been open about wanting Ondas to be a consolidated platform rather than a collection of parts. The reported $20 billion line tells you the ambition. It does not tell you the timeline, the dilution required to get there, or whether the backlog converts to revenue on schedule. Those three things, not the quote, will decide what ONDS shareholders actually earn from here. We will keep tracking all three.

Sources

- David Ben Ishay, public LinkedIn post describing the investor call (translated; his account, not independently verified)

- Investing.com, Ondas subsidiary partners with Lockheed Martin on drone defense (June 23, 2026)

- Investing.com, Ondas CEO Eric Brock sells $31.9M in company stock (June 2, 2026 Form 4 coverage)

- Fintel, ONDS short interest data (167.5 million shares short, 33.29% of float)

- ChartExchange, ONDS borrow fee (3.74% as of July 1, 2026, via Interactive Brokers)

- Prices and market cap from consolidated exchange closing data, July 1, 2026.

This is general market commentary and opinion, not investment advice. The $20 billion remark is one call participant's translated account and has not been independently verified. Prices are July 1, 2026 closing prices and will move. Markets can go down as well as up, and you can lose money. Always do your own research and consider speaking with a licensed financial professional before making any investment decision.