Key points

- The Roundhill Memory ETF (DRAM) added GigaDevice Semiconductor at a 2.91% weight, its first-ever Chinese holding.

- The "China is cheap" instinct is backwards here: GigaDevice trades at a forward P/E near 65x, versus single digits for Micron (MU) and SK Hynix.

- SK Hynix, Samsung and Micron (MU) still dominate the fund at roughly 25% each once swaps are counted, leaving GigaDevice a sub-3% sliver at the bottom.

- China's real DRAM giant, CXMT, is still private (a roughly $4.3B Shanghai IPO is due in late 2026), so the fund cannot own it yet.

- GigaDevice and CXMT share founder Zhu Yiming and a roughly $825M DRAM supply deal, so GigaDevice is the closest listed proxy for still-private CXMT.

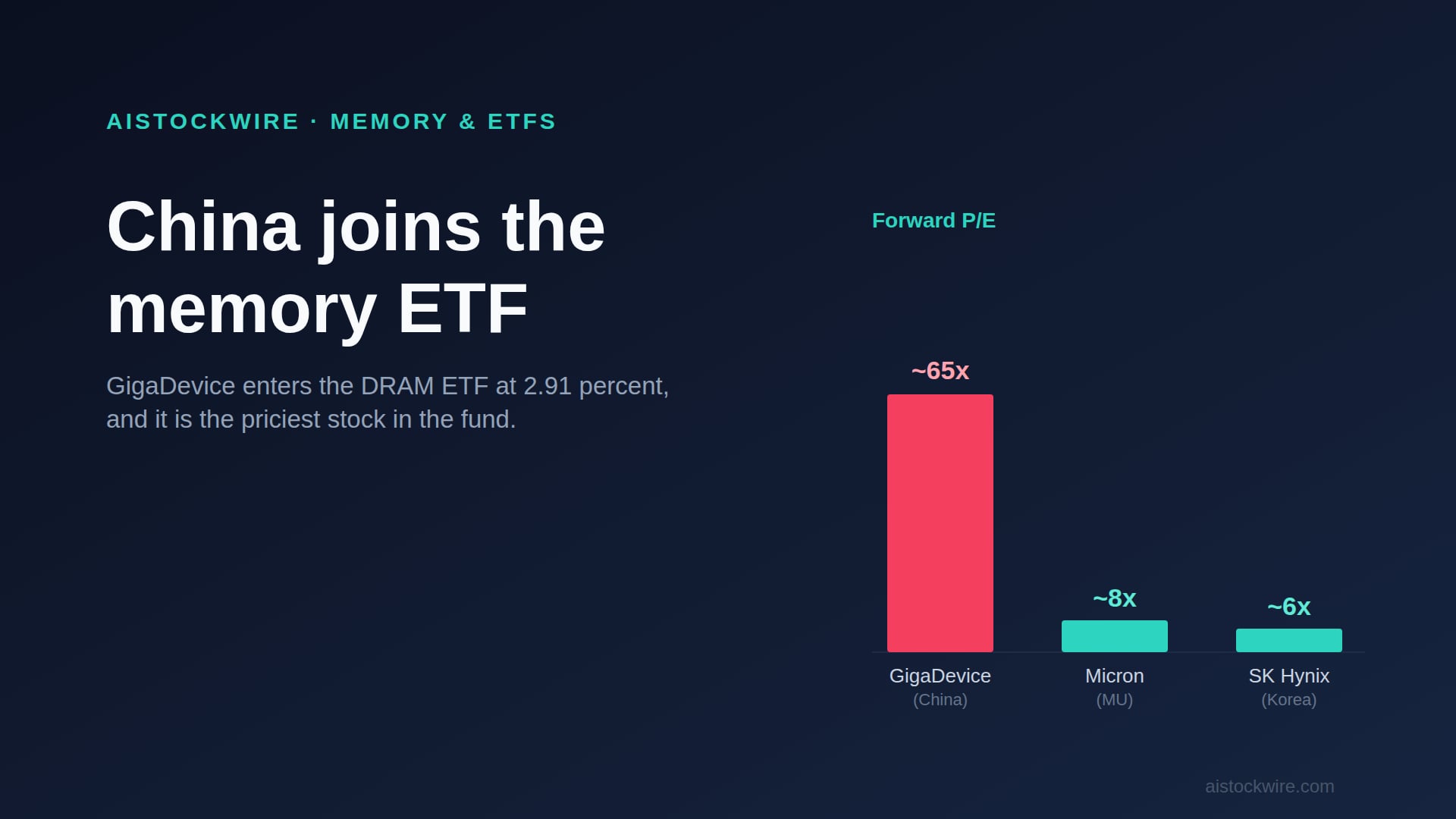

The Roundhill Memory ETF, which trades under the ticker DRAM, has spent its short life as a clean bet on the AI memory boom: Korea's SK Hynix and Samsung up top, then the storage and flash names underneath. This week it did something new. It added GigaDevice Semiconductor, a Beijing chipmaker, at a 2.91 percent weight. It is the first Chinese company the fund has ever held. And if your first instinct is "good, finally some cheap China exposure," the numbers are about to surprise you.

What GigaDevice actually is

GigaDevice is not really a DRAM company, at least not mainly. It is the world's number two maker of NOR flash, a kind of memory used in cars, appliances and industrial gear, with about 18.5 percent of that market. It also makes microcontrollers, sensors, some NAND flash, and a slice of specialty DRAM. It is one of China's larger listed chipmakers, trading in Shanghai and, since January, in Hong Kong, where it jumped nearly 40 percent on its first day. So it earns a place in a memory fund, but it is a flash-and-controllers story far more than a DRAM one.

The part that flips the "cheap China" idea

Here is where it gets interesting. The assumption that Chinese tech is the cheap option does not hold for this stock at all. GigaDevice trades at a trailing price-to-earnings ratio well north of 100, and even on next year's expected earnings it sits around 65 times. Compare that with the giants that make up most of the fund. Micron (MU) and SK Hynix both trade for roughly 20 to 25 times trailing earnings, and single digits looking forward. In other words, the newest and smallest name in the basket is also, by a wide margin, the most expensive one in it.

Why so pricey? China's drive for chip self-sufficiency has turned its domestic semiconductor names into momentum favorites, and mainland retail investors will pay almost anything for a company tied to that story. You are not buying a discount here. You are buying a national-priority narrative at a steep premium.

Cheap chips, expensive stock

The confusing part is that the "cheap" instinct is half right, just pointed at the wrong thing. Chinese memory is cheap where it actually counts, on the price tag of the chips themselves. Makers like GigaDevice, and the bigger CXMT, win market share by undercutting everyone else on older-generation DRAM and flash. That is exactly the kind of pricing pressure that can eat into the fat margins the rest of the fund is enjoying right now. So you end up with an expensive equity wrapped around a cheap product, and the cheap product is a threat to the 90 percent of the ETF that is not Chinese. That is a strange thing to own inside one ticker.

The bigger China name the fund still cannot touch

If you actually wanted Chinese DRAM, GigaDevice is not the main event. That title belongs to CXMT, or ChangXin Memory Technologies, which is China's largest DRAM maker and now ranks around fourth in the world with roughly 8 percent of the global market. The catch is that CXMT is still private. It has approval for a Shanghai STAR Market listing later this year, aiming to raise about $4.3 billion, and its first-quarter revenue reportedly jumped more than 700 percent from a year earlier. Until that deal actually prices, an index fund like this one has no clean way to own the real Chinese DRAM champion, which is a big part of why GigaDevice got the call instead.

GigaDevice and CXMT are not strangers

Here is the twist that is easy to miss: these two are joined at the hip. Both were founded by the same person, Zhu Yiming, who started GigaDevice in 2005 and later founded CXMT in 2016, where he is still chairman and CEO. GigaDevice was an early backer of CXMT, and the two now run a clear division of labor: CXMT manufactures the DRAM, and GigaDevice handles the product development and the selling. GigaDevice has even lined up about $825 million of DRAM purchases from CXMT and its parent company this year. So while you still cannot buy CXMT directly, owning GigaDevice is the closest thing to a backdoor on it that public markets offer right now. The one Chinese DRAM name in the fund you can buy is tied to the one you cannot.

What else is in the fund

The headline weights here are a little deceptive, because the fund leans heavily on swaps. Buying shares of giants like Samsung and SK Hynix directly is harder than it sounds when they are foreign-listed, so the ETF picks up much of that exposure through total-return swap contracts backed by Treasury bills. Once you count those swaps next to the direct shares, the real shape of the fund is three roughly equal giants at the top: SK Hynix, Samsung and Micron each land close to a quarter of it, or about three-quarters of the fund between them. Below that sit the storage and flash names, with Sandisk around 5 percent, Kioxia near 4.7, and Western Digital and Seagate around 4 each. The genuine small fry are the specialty makers, Taiwan's Nanya Technology and Winbond, and now GigaDevice at about 2.7 percent (it came in at 2.91 and has drifted a little with the share price since). So GigaDevice is not pushing anyone important aside. It is a toe in the water at the very bottom of the roster. The ETF itself has pulled in billions of dollars since its April debut and, after this week's memory selloff, trades around $72, down from a peak above $81 but still well up from the $28 it started at.

So is it a good addition?

On balance, adding a Chinese name is defensible and probably overdue. China is building memory capacity at a pace nobody can afford to ignore, and a fund that calls itself the memory ETF looks incomplete with no China in it at all. GigaDevice is a real leader in its niche and an easy, liquid way to get that exposure without wrestling with A-share access yourself.

The caveats are just as real. At under 3 percent, it barely moves the fund either way, so do not expect it to change your returns. You are adding the single most expensive stock in the basket, priced in a market with its own rules around foreign ownership and sitting in the middle of a US-China chip fight that can flare up without much warning. And the CXMT connection only goes so far. GigaDevice is an indirect, second-hand line to China's DRAM champion, not the champion itself, which is still waiting on the sidelines to go public.

None of this is investment advice. But if you own DRAM, or you are weighing it, the GigaDevice add is a small, smart-sounding move with a big asterisk: the cheap-China trade and the expensive-China stock are not the same thing, and this is the expensive one.